Setting the Stage: Pre-WASDE Expectations

A hot and dry August led to lower, but wide-ranging yield estimates for soybeans and corn ahead of the

September World Agricultural Supply Demand Estimates (WASDE). Through the week of September 10, only

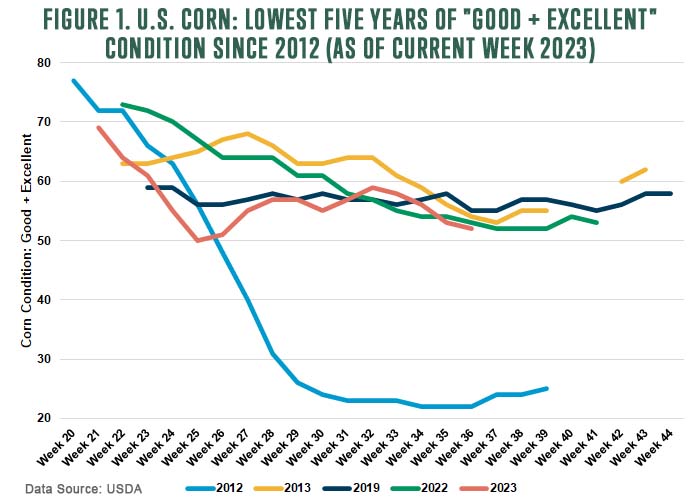

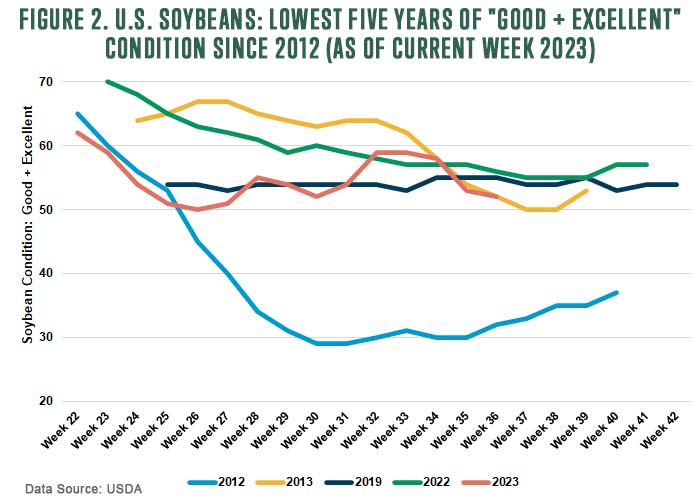

52% of the corn and soybean crop was rated as “good to excellent.” U.S. growers have to go back to 2012 to find

a crop with a worse “good to excellent” rating.

Ahead of the September WASDE, market averages pegged corn yields at 173.3 bushels per acre and soybean

yields at 50 bushels per acre. Estimates for both crops were lower compared to the August WASDE. Table 1

summarizes pre-report estimates ahead of the September WASDE for both corn and soybeans.

Table 1. U.S. Corn and Soybean Pre-Report Estimates |

|---|

Corn |

| Average | Range | USDA August |

|---|

| Yield | 173.3 | 171 - 175 | 175.1 |

| Production | 14,994 | 14,762 - 15,125 | 15,111 |

| Ending Stocks | 2,127 | 1,830 - 2,399 | 2,202 |

Soybeans |

| Average | Range | USDA August |

|---|

| Yield | 50 | 49 - 51 | 50.9 |

| Production | 4,139 | 4,056 - 4,218 | 4,205 |

| Ending Stocks | 213 | 170 - 255 | 245 |

| Source: Compiled from Wall St. Journal |

An already tight soybean crop was expected to come in 32 million bushels lower than August projections for a

total ending stock of 213 million bushels, the lowest level since marketing year 2015/16. Ending stocks for corn,

by comparison, were expected to be at their highest level since marketing year 2013/14, with high corn acres

offsetting lower yields.

So how did expectations align with the USDA’s September WASDE?

Corn Outlook: Larger Supplies, Higher Ending Stocks, and Unchanged Use

- USDA lowered corn yields by 1.3 bushels per acre to 173.8 bushels per acre.

- The U.S. corn crop is projected to produce more than 15.13 billion bushels this year, second highest only to 2016/17.

- Corn plantings for 2023/24 corn adjusted upward 0.8 million acres to 94.9 million acres, the highest since 2013/14. As a result, harvested area increased from 86.3 million acres from the August WASDE to 87.1 million acres.

- Demand on the balance sheet for 2023/24 was unchanged from August at 14.4 billion bushels. Ending stocks increased 19 million bushels to 2.2 billion bushels.

What this means for corn producers

The 2023 corn market has been marked by volatility. However, corn looked bearish at the onset of the crop year, and remained bearish in the September WASDE.

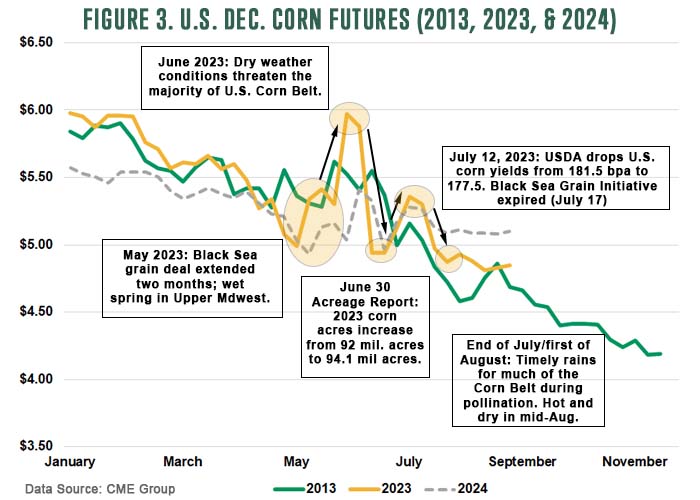

While USDA reported lower corn yields, its projections were slightly above the market expectations – 173.8 vs. 173.3 acres per bushel. At the same time, USDA increased plantings and harvested area. Taken as a whole, USDA projects higher production levels. Figure 3 compares the trend of December 2023 corn futures to 2013, a time when the U.S. corn crop significantly rebounded because of larger plantings.

While supply increased, demand remained unchanged. Projections for ending stocks have risen to 2018/19 levels.

It’s important to note that USDA pegged ending stocks 94 million bushels higher than the market’s pre-report average expectation but still within the overall range. At the time of the September WASDE’s release, December 2023 corn was down approximately $0.08 per bushel and closed down approximately $0.09 to $4.77 per bushel.

The stocks-to-use ratio rose to 15.4 percent. If realized, this would be 3.2 percentage points higher than the 10-year average and the highest since 2018/19. The projected season-average farm price of $4.90 per bushel was unchanged from August. Increased demand continues to be key to the corn balance sheet. Meanwhile, exports remain sluggish on lower Chinese demand and the strength of the U.S. dollar.

World ending stocks were increased 2.9 million tons to 314 million tons. This was due to increased production from the U.S., Brazil, Mexico, China and Ukraine. Despite war, Ukraine is expected to see higher yields. However, corn production for the country is 18% below its five-year average and 6.6% below the 10-year average. Production for the European Union was mostly unchanged from August.

The world stocks-to-use ratio for 2023/24 increased from 25.9% to 26.2%. This is still 1.6 percentage points below the 10-year average and the global corn situation remains tight.

Soybean Outlook: Lower Beginning Stocks, Production, Crush, Exports, and Ending Stocks

- USDA reduced soybean yields 0.8 bushels from last month down to 50.1 bushels per acre. This was slightly higher the market’s pre-report average by 0.1 bushels per acre.

- The drop in yields lowered 2023/24 soybean production 95 million bushels down to 4.2 billion bushels, 2% lower than 2022/23.

- USDA also slightly increased plantings and area harvested by 100,000 acres to 83.6 million and 82.8 million, respectively.

- Soybean production was lowered 59 million bushels to 4.1 billion as lower yields offset higher harvested area. This level of production would be the lowest since 2019/20 and 1% lower than the 5-year average.

- 2023/24 soybean supplies are projected at their lowest level since 2015/16. With lower soybean supplies, USDA lowered exports by 35 million to 1.79 billion bushels, 8% below the 10-year average. Additionally, despite crush being lowered 10 million bushels to 2.29 billion, it would still be a record high if realized.

- With lower supplies, ending stocks for 2023/24 were lowered 25 million from last month to 220 million bushels. This would be the lowest ending stocks level since 2015/16 and 36% below the 10-year average.

What this means for soybean producers

The September WASDE was bearish for soybeans, with USDA reporting more soybeans than the market expected. Despite the bearish tone, the domestic balance sheet remains tight.

On release of the report, November 2023 soybeans dropped $0.11 per bushel and closed down $0.24 per bushel to approximately $13.45 per bushel.

The 2023/24 stocks-to-use ratio at 5.2% remains below its 10-year average of 8.4%. If realized, the 2023/24 stocks-to-use ratio would be the lowest since 2015/16. It’s becoming clear that lower supplies are driving lower usage.

USDA increased the U.S. season average farm price by $0.20 per bushel to $12.90 based on tight supply.

By comparison, the global soybean market remains abundant. The global stocks-to-use ratio was increased slightly from 30.9% to 31%, which is well above the 10-year average of 27.4%. Globally, Ukrainian soybean production was increased. But global soybean crush was decreased 1.8 million tons to 327.7 million on lower crush from Argentina, Pakistan, the European Union, Thailand and the U.S. Argentina is significant; its crush was reduced 1.8 million tons to 34.5 million on lower expected supplies over the next several months.

Despite a reduction of 0.2 million tons to 119.2 million, global ending stocks are expected to hit a record of more than 5 million metric tons.

Slight adjustments to soybean yields could significantly change the soybean balance sheet. It is never too early to consider how today’s market situation might influence 2024 decisions.

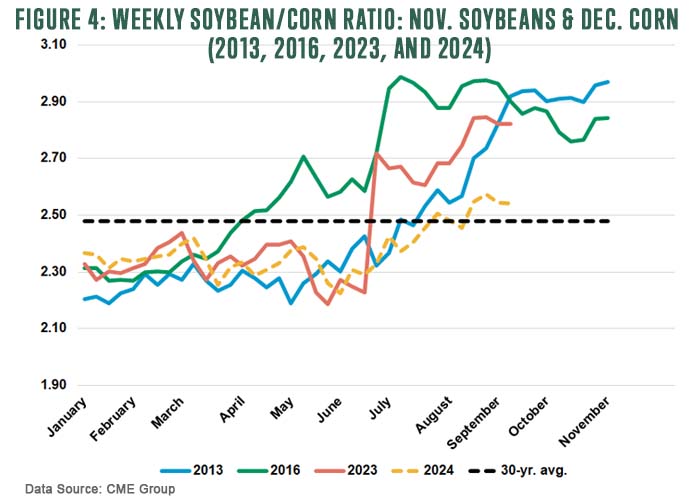

As Figure 4 shows, since USDA’s June 30 Acreage Report, futures prices have signaled that the market needs soybeans. The illustration shows the weekly soybean-to-corn price ratio for November soybean futures and December corn futures for 2013, 2016, 2023, and 2024. A higher ratio signals that relative profitability for soybeans may be greater than that of corn.

As Figure 4 shows, since USDA’s June 30 Acreage Report, futures prices have signaled that the market needs soybeans. The illustration shows the weekly soybean-to-corn price ratio for November soybean futures and December corn futures for 2013, 2016, 2023, and 2024. A higher ratio signals that relative profitability for soybeans may be greater than that of corn.

Today, the ratio stands at more than 2.8, well above the 30-year average and roughly in line with 2013 and 2016. In each subsequent year, 2014 and 2017, soybean plantings increased significantly. In fact, the 2017/18 marketing year saw soybean plantings exceed 90 million acres.

Like futures prices, the soybean-to-corn price ratio for 2024 is signaling the market’s need for soybeans. Does that mean that producers intend to plant more soybeans next year? Possibly.

But it’s early and today’s market environment could adjust. While soybeans are tight domestically, they are abundant globally. The opposite is true for corn.

Keep an eye on these trends in the months ahead.

Wheat Outlook: Domestic Balance Sheet Unchanged; World Ending Stocks Reduced

- The unchanged ending stocks level at 615 million bushels was in line with market expectations. If realized, 2023/24 ending stocks would be 30% below the 10-year average.

- The global wheat outlook calls for lower supplies, consumption, exports, and ending stocks.

- Global supplies were lowered 7.2 million tons to 1,054.

- World ending stocks were reduced 7 million tons to 258.6 million.

What this means for wheat producers

At a high level, the domestic balance sheet remained unchanged for wheat. As a result, USDA left the 2023/24 average farm price unchanged at $7.50 per bushel and the all-wheat stocks-to-use ratio at 33.6%. If realized, this would be 9.4 percentage points below the 10-year average of 43%.

However, the reduction in global ending stocks provided some bullish sentiment to the wheat market. The world balance sheet already was tight. And it just got tighter with continued war in Ukraine and dry growing conditions in counties such as Australia, Canada, Argentina, and the European Union. In drought-impacted Australia, wheat production was lowered 3 million tons to 26 million, a decline of about 34% from last year and that country’s lowest production since 2019/20.

With the USDA’s September adjustments, world ending stocks would be at their lowest level since 2015/16. The global stocks-to-use ratio was reduced from 33.4% in August down to 32.5%. This would be the lowest world stocks-to-use ratio since 2014/2015 and 2.9 percentage points below the 10-year average.