USDA lowered its yield projection for corn and soybeans in the World Agricultural Supply and Demand Estimates (WASDE) for August. The revision was expected. However, yield projections for both commodities came in below the market’s average expectation.

Ahead of the August WASDE, the market estimated corn yields would drop to an average of 175.4 bushels per acre, down 2.1 bushels from the July WASDE. The USDA revised its estimate to 175.1 bushels per acre.

Soybean yield was expected to be slightly lower than the July estimate at 51.2 bushels per acre. USDA’s August estimate was 50.9 bushels per acre. With the marketing year 2023/24 soybean balance sheet already tight, any further downside adjustment to yield would be significant.

The table below summarizes the market’s expectation ahead of the August WASDE for both yield and production for corn and soybeans.

U.S. Corn and Soybean Production Estimates (Pre-August WASDE) |

|---|

| Average | Range | USDA July |

|---|

| Corn Yield | 175.4 | 172.4 - 178 | 177.5 |

| Corn Production | 15,126 | 14,885 - 15,361 | 15,320 |

| Soybean Yield | 51.2 | 50.1 - 52 | 52 |

| Soybean Production | 4,238 | 4,140 - 4,299 | 4,300 |

| Data Source: USDA |

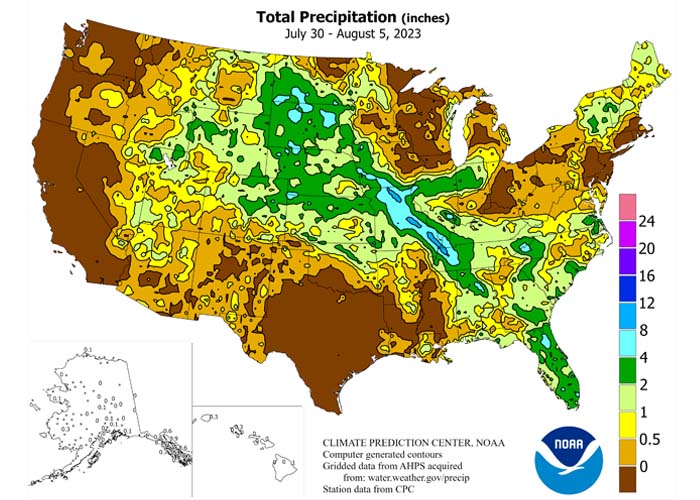

The market expectation for slightly lower yields was justified given the hot and dry month of June. However, timely rains across much of the Corn Belt during the last week of July through the first part of August improved corn and soybean conditions. As of July 4, drought conditions were reported on 67% of corn and 60% of soybean acres. As of August 8, drought conditions had improved, impacting 49% of corn acres and 43% of soybeans. The map on the bottom left shows total accumulated precipitation between July 30 and August 5.

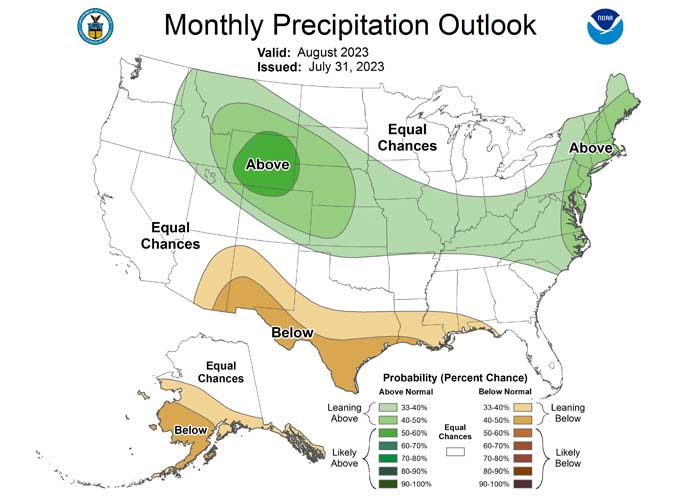

The early August precipitation could prove timely. This period is peak pollination for corn. For soybeans, August rains generally bring September yield gains. Fortunately, the rest of August holds a slight to above-average chance of precipitation for much of the Corn Belt.

Both the corn and soybean crops will continue to remain in a weather market until the combines start and harvest is ready to roll.

Corn Outlook: Reduced Supplies, Lower Domestic Use, Smaller Exports, and Tighter Ending Stocks

- The U.S. corn crop is projected to produce 15.1 billion bushels this year. If realized, production would be 10% higher than the 2022/23 marketing year and second only to 2016/17.

- USDA’s lower yield estimate of 175.1 bushels per acre dropped total corn production to 209 million bushels from July’s projection. But 2023 corn acres, at 94.1 million, would be the third highest since 1944.

- Based on the USDA Crop Production report, five states have yield forecast above last year: Indiana, Iowa, Nebraska, Ohio and South Dakota. Yields in Illinois, Minnesota and Missouri are forecast below a year ago.

- Demand on the balance sheet for 2023/24 was lowered 95 million bushels from July. Most notably, corn exports continue to slump. USDA lowered corn exports by 50 million bushels.

What this means for corn producers

The August WASDE was mostly “as expected” for corn, despite USDA being lower on their yield estimate compared to the market’s expectation. In addition, USDA’s reduction in demand helped elevate ending stocks above the market’s expectation. The average market estimate ahead of the report pegged 2023/24 ending stocks at 2.179 billion, whereas USDA’s projection puts ending stocks at 2.2 billion bushels. December 2023 corn closed down $0.09 to $4.87 per bushel.

Domestic ending stocks for 2023/24, at 2.2 billion bushels, are about 27% above their 10-year average. If demand remained constant, yields would need to drop to 169.7 bushels per acre to return to the 10-year average. Aligned with previous months, the U.S. is expected to have a lot of corn.

The stocks-to-use ratio of 15.3% is the highest since 2018/19, contributing to a projected season-average farm price of $4.90 per bushel. Increased demand will continue to be key to the balance sheet.

The global situation remains different from the domestic picture as supplies remain tight. Foreign production is expected lower in the European Union, China and Russia, with increases for Ukraine and Canada. Corn production for Ukraine is projected higher as a result of timely rain and lower temperatures. However, corn production in Ukraine remains 20% below the country’s five-year average and 10% below the 10-year average. With USDA lowering global ending stocks by 3 million metric tons, the world stocks-to-use ratio, at 25.9%, is 1.9 percentage points below the 10-year average.

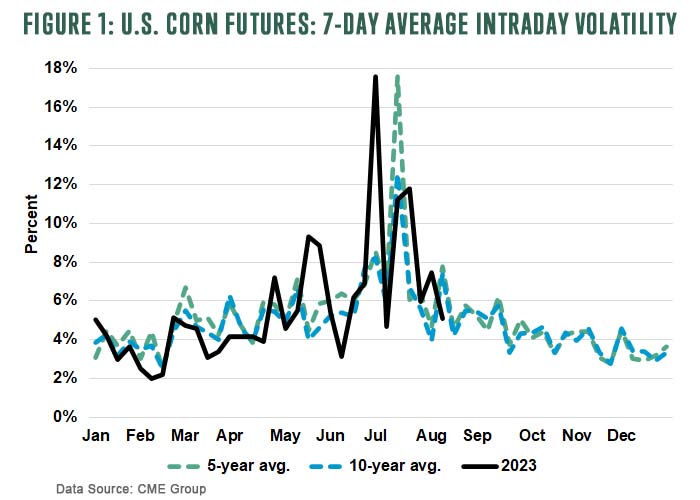

Moving forward, the corn market will continue to be weather dependent. Since their June high, corn futures have traded volatile while trending lower.

Moving forward, the corn market will continue to be weather dependent. Since their June high, corn futures have traded volatile while trending lower.

Figure 1 shows the seven-day average intraday volatility for corn futures in 2023 and compares it with five-year and 10-year averages. Late spring to mid-summer mark the largest volatile swings in corn prices. This is the result of many factors, including old stock supply and uncertainty about new production. These tend to be the months with the greatest potential for market opportunity. For 2023, significant market opportunities existed for producers to take advantage of upside volatility in the market.

Prices tend to be less volatile between early and late summer into fall as expectations for the corn crop become known. While peak upside may have passed in June and July, continued war escalation in Eastern Europe, tight global supplies, and a surprise August weather event could provide market opportunities heading into harvest.

Soybean Outlook: Higher Beginning Stocks, Lower Production and Exports

- USDA reduced soybean yields 1.1 bushels from last month down to 50.9 bushels per acre, dropping 2023/24 soybean production 95 million bushels to 4.2 billion bushels. If realized, this would be 2% lower than 2022/23.

- Soybean supplies for 2023/24 are projected at their lowest level since 2019/20. On expectation of lower supply, USDA also cut exports by 25 million to 1.875 billion bushels, 7% below the 10-year average. Soybean crush was left unchanged, which if realized, would be a record high.

- With lower supplies only partly offset by reduced use, ending stocks for 2023/24 were lowered 55 million to 245 million bushels. If realized, this would be the lowest ending stocks level since 2015/16 and 6% below the 10-year average.

What this means for soybean producers

The August WASDE was “as expected,” but slightly bullish for soybeans. Markets were expecting slightly higher yields and ending stocks than USDA’s projection. Based on lower supply and higher than average demand, USDA increased the U.S. season average price by $0.30 to $12.70 per bushel.

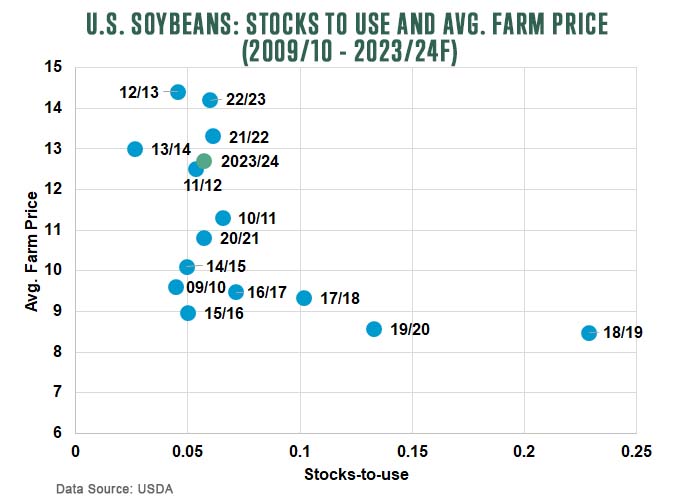

The domestic soybean market is projected to remain tight. The 2023/24 stocks-to-use ratio at 5.8% remains below its 10-year average of 8.4%. By comparison, the global soybean market remains abundant. The global stocks-to-use ratio at 30.9% is well above its 10-year average of 27.4%. Globally, there were few significant changes with USDA lowering world ending stocks 1.6 million metric tons to 119.4 million metric tons. However, if realized, this level of ending stocks globally would be a record high by more than 5 million metric tons.

August rains will be key going forward for the soybean balance sheet. Any further downward adjustment to soybean yields could make the balance sheet extremely tight and cause demand to pull back further as crush and exports continue to fight for bushels. Holding demand constant from the August balance sheet, a yield reduction of just one bushel per acre would lower the stocks-to-use ratio to 3.8%. However, it is also possible to see an additional yield increase to soybeans in September, especially with the rains seen so far in August. A yield increase of one bushel and holding demand constant would increase the stocks-to-use ratio to 7.7%. Slight adjustments to soybean yields moving forward can make a significant difference to the soybean balance sheet.

Wheat Outlook: Decreased Supplies, Lower Domestic Use, Reduced Exports, and Higher Stocks

- USDA decreased its all-wheat production estimate for 2023/24 by 5 million to 1.734 billion bushels, the highest level since 2020/21 and up 5% from 2022/23. This was slightly below the market’s pre-report expectation of 1.74 billion bushels. All-wheat production was lowered due to a 0.3 bushel per acre yield reduction to 45.8 bushels per acre.

- USDA lowered domestic usage by 3 million bushels from July’s report, while exports fell 25 million to 700 million bushels due to slow export pace. With total wheat use projected at 1.829 billion bushels, this would be the lowest level of usage since marketing year 1976/77.

- U.S. wheat ending stocks for 2023/24 rose 23 million bushels to 615 million bushels, well above the market’s average pre-report expectation of 594 million bushels. Despite ending stocks coming in above expectations, they’re still projected 30% below the ten-year average.

- The major changes to wheat from the report came from the global balance sheet. Due to drought in many wheat producing countries, wheat production was lowered in the European Union by 3 million metric tons to 135 million metric tons; Canada by 2 million metric tons to 33 million metric tons; and China by 3 million metric tons to 137 million metric tons. While wheat production was raised in Ukraine and Kazakhstan, the net effect saw world wheat ending stocks fall from 266.5 million metric tons in July to 265.6 million metric tons in August. If realized, this would be the lowest level of world wheat ending stocks since 2015/2016.

What this means for wheat producers

In many ways, wheat experienced the most changes from the August WASDE. With domestic ending stocks projected higher than the market’s expectation, the report was slightly bearish for wheat. However, lower global ending stocks provided some bullish sentiment to the market.

USDA left the 2023/24 average farm price unchanged at $7.50 per bushel. The 2023/24 all-wheat stocks-to-use ratio is projected at 33.6%, almost 3 percentage points higher than 2022/23, but remaining well below the 10-year average of 43%.

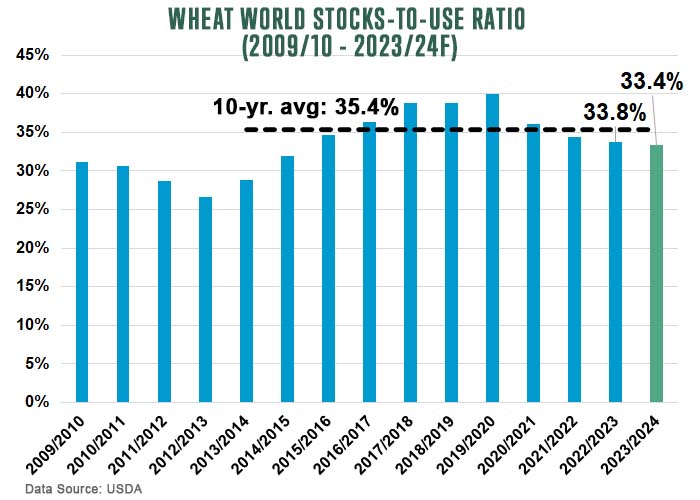

Globally, the balance sheet remains tight. While world ending stocks are projected to be at their lowest since 2015/16, the global stocks-to-use ratio at 33.4% would be the lowest since 2014/2015. Despite USDA increasing Ukrainian wheat production by 3.5 million metric tons to 21 million metric tons, it remains 21% below their 5-year average and 20% below their 10-year average. The wheat balance sheet, domestically and internationally, remains tight. As a result, the wheat market will continue to remain volatile given the ongoing war between Russia and Ukraine.