The inverse thrills of the past year will be remembered by many livestock market participants. Cattle, hog and poultry producers all had their share of adversity and resulting market turbulence.

Avian influenza ran riot through turkey and egg houses and pork producers saw a slingshot effect that carried production to record levels and prices to four-year lows as output more than recovered from the 2013-14 bout with porcine epidemic diarrhea virus. Fed-cattle prices set new records on short supply only to plunge by $21/cwt. in the course of six weeks, a magnitude of loss for that length of time exceeded only in 2004 - during the mad cow crisis. Even dairy producers saw market volatility.

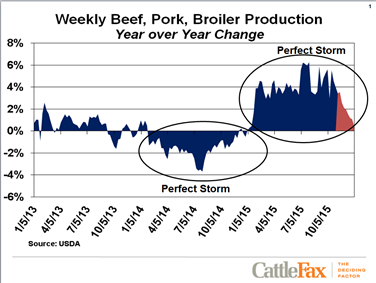

“The livestock industry experienced back-to-back extremes,” said Jud Jesske, Frontier Farm Credit vice president of agribusiness lending with an emphasis on beef producers. As can be seen in the chart below, weekly total meat production swung from as much as four percent below a year earlier during 2014 to better than 6 percent above in 2015.

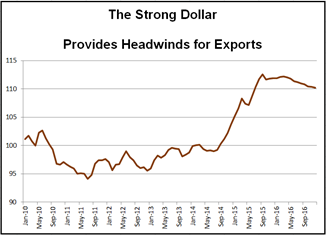

The strong dollar doesn’t help. Based on USDA’s agricultural trade-weighted index, USDA’s index began its upward sprint in August 2014. By the end of the year, it was 10 percent above a year earlier. While foreign exchange rates are far from the only factor affecting exports, it is widely agreed that a strong dollar makes U.S. products more expensive in global markets.

Data: USDA/ERS

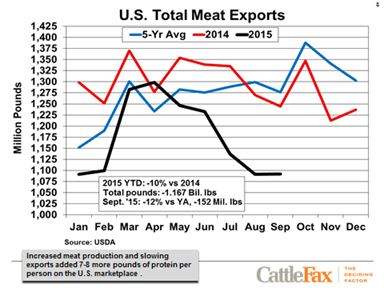

Total U.S. meat exports plummeted beginning in May 2015 (see chart below), and the 2015 total is estimated to be down 1.3 billion pounds from 2014, bolstering domestic supplies by a like amount, according to CattleFax That is the largest one-year drop, with the exception of 2004 in the wake of bovine spongiform encephalopathy.

From May 2015 to October 2015, beef exports slumped by more than 30 percent to their lowest level in 20 months. Pork exports recovered from the plunge seen during the trough in supply due to PEDv. But in November 2015, they fell 18 percent below the same month in 2014. Broiler meat exports also have slipped by almost a quarter from year-ago levels.

Cheap corn = more meat

Adding to the supply, production rose dramatically as both cattle and hog weights climbed. Combined with slower exports, the net meat and poultry supply in the United States increased nearly 4.5 billion pounds from 2014 to 2015, the largest yearly increase in almost 40 years. Looking at the past decade, meat supplies rose from the third smallest in 2014 to the largest in 2015.

“Many of our customers felt the effects of the disease outbreaks and the resulting market gyrations,” says Marshall Hansen, vice president of Frontier Farm Credit Agribusiness Finance (ABF). “However, volatility is a fact of life in agriculture. And while it was exceptionally high in 2015, most of the operations we work with were in a good position to deal with it.”

Several ABF customer operations hit by the deadly bird flu HPAI H5N1 lost months of business and were forced to lay off employees, but are now rebuilding flocks. Case Gabel, a young Nebraska cattle feeder, notes that “cattle equity swings on a weekly basis have been unprecedented. But forward crush margins are as healthy as we’ve seen in several years and futures and options allow us to minimize financial risk.”

As the year drew to a close, the market looked as if it might improve following the quarterly hogs and pigs report and monthly cattle on feed report, both of which indicated slightly tighter supplies than were expected. Heading into 2016, we will share additional insights into each of the livestock markets, beginning with the impacts of HPAI.